Did you know you can still make strategic decisions that impact your 2019 taxes? Contributions to certain accounts allow special time-bending tax treatment. Power Up your tax strategy by considering the following strategies that may reduce your taxes, or be more tax-efficient.

Retirement Account Contributions Tax Filing strategies

Make your retirement account contributions travel back in time!

It’s 2020, but you may be able to apply your contribution to 2019 still. Identify your contributions to be for the tax-year 2019 and make the contributions by April 15th, 2020.

Traditional IRA

Deductible Contributions

Deductible contributions to a traditional IRA will reduce your taxes and potentially increase your refund. Traditional IRAs allow the growth of your investments to grow tax-free, but you will pay taxes when you ultimately begin to withdraw funds in retirement.

Traditional IRA’s are mostly available to individuals and spouses who do not have access to a retirement account through their employer. If you have access to an employer retirement plan, you may still be eligible to make deductible Traditional IRA contributions, but there are income phaseouts to be aware of.

Non-Deductible Contributions

It’s important to know that even if your income phases you out of “deductible” IRA contributions, you can still make “non-deductible contributions”.

Non-deductible contributions do not reduce your taxes, instead, those funds can be withdrawn tax-free in the future. The growth on these non-deductible contributions is not tax-free though. Instead, the growth of non-deductible IRA contributions is taxable when withdrawn. You want to keep track of your non-deductible contributions.

Why would you do a “non-deductible” contribution? Most of the time this happens on accident and people don’t realize it. There is actually an advanced strategy where this can be a powerful loop-hole. It’s called a “back-door Roth Conversion”.

The back-door Roth conversion allows high-income individuals and families to avoid the income phase-outs of Roth contributions.

Roth IRA

Roth contributions do not reduce your taxes. Instead, your contributions are allowed to grow tax-free and can be withdrawn tax-free. This is a great option for you if you are early in your career and you anticipate a significant pay increase that will push you into larger tax brackets in the future, especially when you retire.

Unlike Traditional IRAs, it does not matter if you or your spouse have access to an employer-provided retirement plan. However, there are still income phase-outs, which is why it’s nice to be aware of the back-door Roth conversion mentioned above.

Simplified Employee Pension (SEP)

This one is for business owners. The employer is the only one who can fund a SEP account and often SEP’s are most heavily utilized by the self-employed due to the extremely high contribution limits. The contribution limit is as much as $56,000 in 2019.

The calculation of how much an employer may contribute is unique though.

An employer can contribute up to 25% of an employee’s gross annual salary or if self-employed, 20% of net adjusted self-employed annual income.

An employer must match employees’ salaries at the same percentage for every employee, which is why this is rarely used by employers with multiple employees, but used often by the self-employed.

Health Savings Accounts Tax-Filing Strategies

If you have an eligible High Deductible Health Plan (HDHP), then you can make deductible contributions into an HSA account.

HSAs receive the best tax-treatment of any type of account. It reduces your tax liability going in, grows tax-free, and can be withdrawn tax-free. Withdrawals need to be for qualified health expenses in order to avoid a 10% withdrawal penalty and being taxed.

If you’ve had medical expenses in 2019 or even early in 2020, you can actually contribute and receive the tax-deduction for 2019 taxes and take out the funds practically the next day to reimburse yourself for qualified health expenses. I’ve used this strategy for both of our children’s birth and only was without the funds for 1 business day.

Accounts You Are Unable to Fund for Previous Tax-Year

401(k)s, 457s, 403(b)s and 401(a)s

Employer-provided retirement accounts do not allow you to travel back in time, which is unfortunate. Employer-provided retirement accounts have significantly larger contribution limits than Traditional and Roth IRAs.

If you felt like you could have contributed more in 2019 to these plans, but forgot to plan it out. Make it a point to build a tax strategy for 2020.

529s

529 contributions do not reduce your federal taxes regardless of when your contributions are made. Instead, some states may allow state income tax deductions for the year contributions are made. Check-out if your state allows for a 529 plan tax deduction.

Withdrawals for qualified education expenses are tax-free. If you have qualified education expenses, you may benefit from contributing and immediately withdrawing the funds if your state provides tax-deductions.

Where Do I Find the Money to Contribute?

Did one of the strategies above catch your eye, but you are scratching your head on how to actually fund a contribution?

First, take inventory.

- Do you have excess savings?

- Do you have non-retirement assets (for many of my clients this is employer stock)?

- Can you use a portion of your refund?

Next, evaluate to what level you can reasonably contribute to these accounts knowing that you cannot access them until retirement or you have qualified medical expenses for the HSA.

- Anything you are able to contribute without putting you in a bind is going to Power Up your financial situation.

- Feel like you could have done better if you planned ahead? I can help.

I Implemented a Tax Filing Strategy, Now What?

It’s a little funky, contributions are not required to be reported until May, but you probably filed in April at the latest. Document your contribution and provide your tax preparer with the details of your contribution. You will receive your 5498 in May, you should share it with your tax preparer so it can be retained in your records.

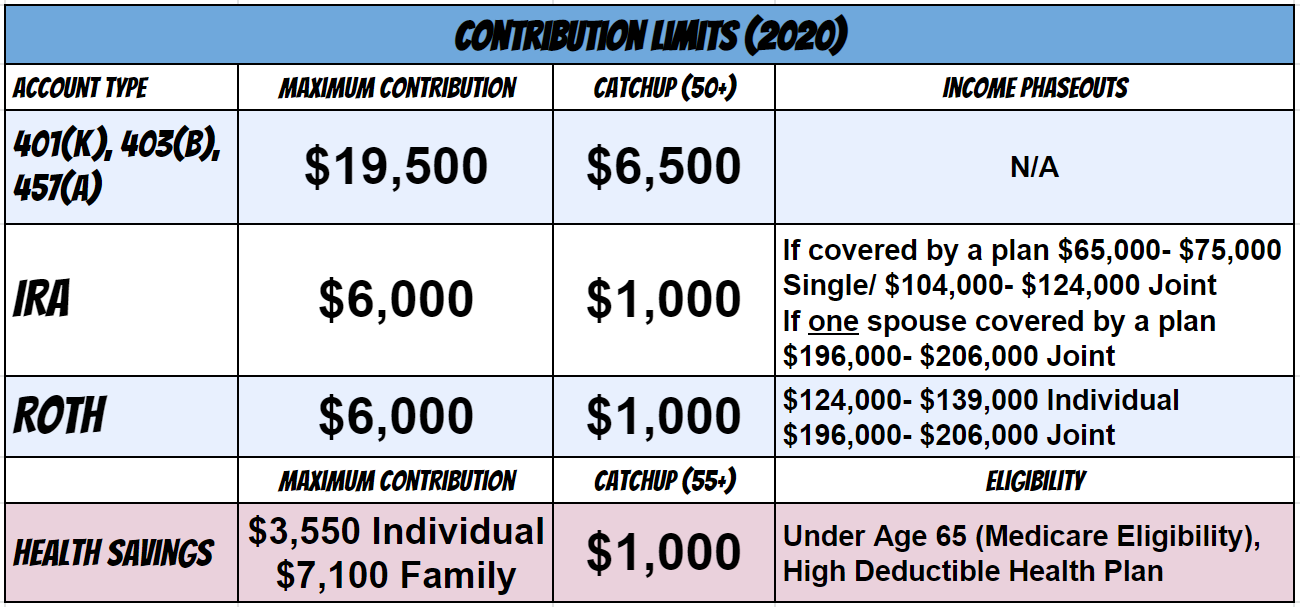

Power Up Your Tax Strategy in 2020

Here are the contributions limits to help you strategize for 2020. The best way to fund these strategies is automatically and monthly.

Are you going to take the challenge to improve upon your 2019 tax strategy? Want to team up? Review our home page for service offerings to determine if we are a good fit.